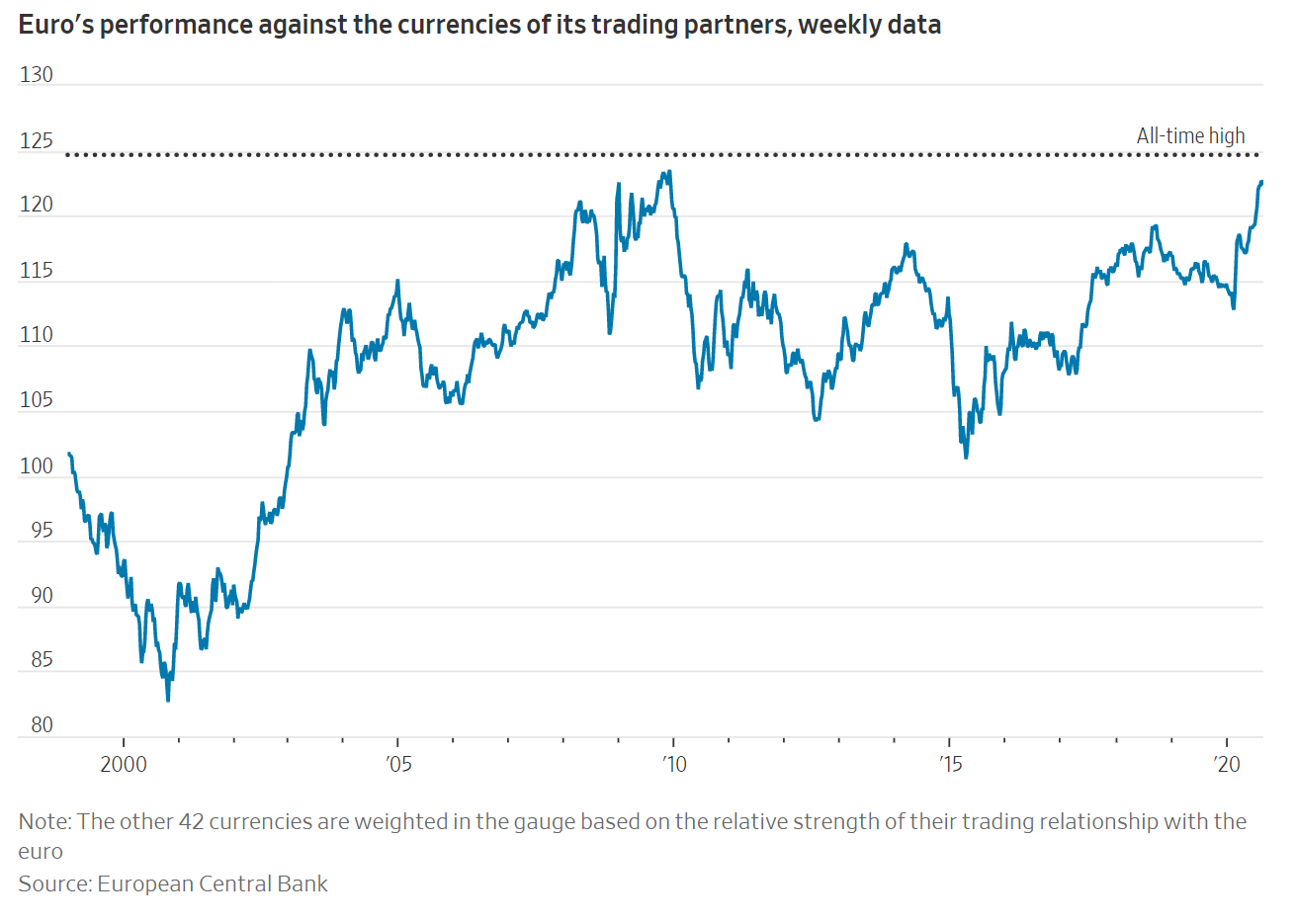

The euro has been surging 10% against U.S. dollar in six months in part because investors think Europe is strongly performing economic rebound after the great lockdown due to pandemic. The bet on European stocks rise has been increased and and investors have kept buying euros in the aspect of optimistic sign of euro-zone recovery. U.S dollar has been weakening in the announcement that Fed will remain its super dovish stance of maintaining federal fund rate near zero until average inflation target(AIT) overshoots over 2% moderately for some time. Please see my blog about it.

https://techongstudy.blogspot.com/2020/08/review-of-monetary-policy-strategy-fed.html

U.S. is still struggling with pandemic now; indicating countermeasures weren't very appropriate enough to flatten the curve. Moreover, uncertainty about new cold war between U.S-China, and anxiety about the presidential election in November makes investors unease. These factors make the dollar weaker than the counter-parties such as Japanese yen and euro.

Eurozone's rapid recovery could be a good sign, however absolute growth alone could stimulate the euro's jump; that means it can hurt inflation target near 2% and European manufacturers from exporting. A strong euro contributes to the risk of deflation or dis-inflation because imported goods become cheaper for European buyers. Moreover, when it comes to export, goods will automatically become relatively more expensive for international customers who pay in other currencies. The price disadvantage will put them in worse condition to compete against foreign rivals.

Even before the pandemic, exports from European started stagnating due to the global slowdown whether it is directly and indirectly affected by the trade tension between U.S. and China. The Trump administration has imposed tariffs to European commodities such as steel and aluminum. Also, spread of Chinese economic deterioration created less demand on European goods. European based companies like Ferrari, Fiat-Chrysler, or Michellin will get profit hit with appreciation of their currency.

“There is a cost to the euro rising, and it’s on earnings,” said Mathieu Savary, a strategist at BCA Research. “If you’re a European industrial company and you compete with Caterpillar, you’re likely to see your profits being hurt when the euro is going up.” Other trading partners including U.S. and China can benefit from strong euro by taking advantage of their relatively weaker currency.

European Central Bank did not change their interest rate at -0.5% and would support €1.35 trillion, equivalent to $1.59 trillion, of eurozone debt under an emergency bond-buying program unveiled in March. The ECB now aims to keep inflation in average of 2%.

Stronger euro is problem to eurozone. It would not meet the target inflation rate and hurt their export industry. However, ECB does not have enough ammunition to lower the key interest rate nor provides fresh new stimulus program, which is already massive. The central bank does not directly target the exchange rate, but should concern about it in regarding to their economy.

Source WSJ, NYT

댓글 없음:

댓글 쓰기